Describing the pharmaceutical industry as one of the greatest risks to society sounds fanciful or the stuff of conspiracy theorists. But demonstrating it’s more theory than conspiracy are the following facts:

- The global pharmaceuticals market is expected to exceed US$1.6 trillion this year

- Just 10 pharma companies (six from the USA, four from Europe) control one-third of the global industry

- Profit margins for drugs are among the greatest of any industry, at around 30% on average

- Predictions suggest that North and South America, Europe and Japan will continue to account for a full 85% of the global pharmaceuticals market well into the 21st century

- One-third of all sales revenues are spent on marketing and this represents about twice the amount spent on R&D.

While the World Health Organization (WHO) is sometimes upheld as party to pharma’s domination, the above facts come directly from the WHO itself.

The WHO first expressed its alleged concern over pharma’s pressure to maintain sales back in 1993, saying it represents “an inherent conflict of interest between the legitimate business goals of manufacturers and the social, medical and economic needs of providers and the public to select and use drugs in the most rational way”.

In light of this, to make various key points about the pharmaceutical industry, with its deeply embedded conficts of interest, we are supporting these points with figures and graphics, rather than words. We’ve derived the figures from Forbes, Deloitte, Statista, the statistics portal that evaluates data and studies from over 18,000 sources.

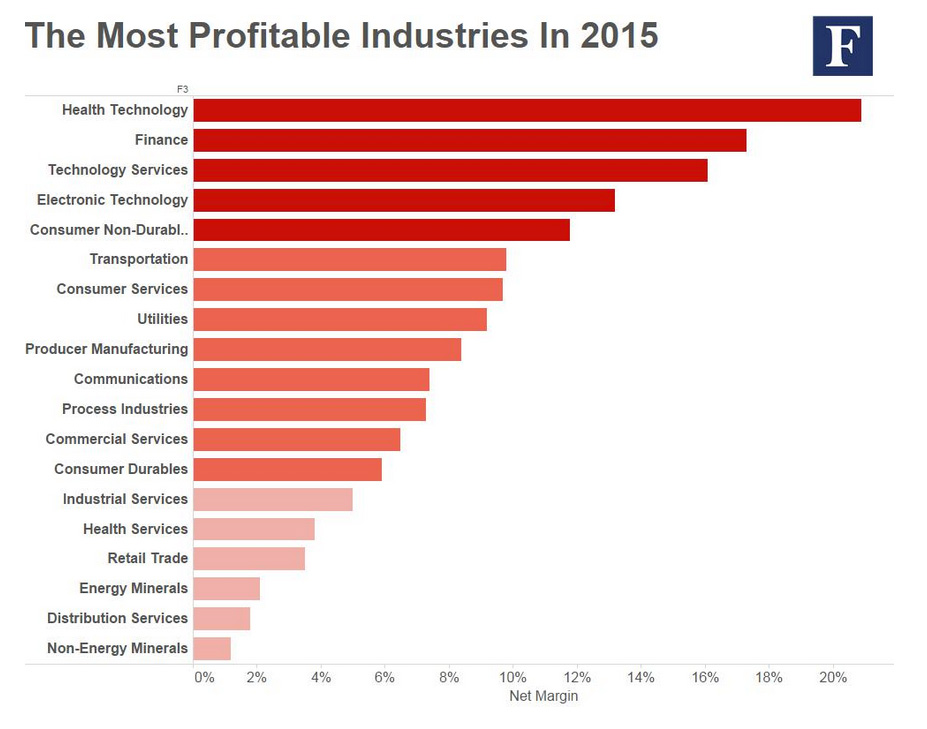

1. The pharmaceutical industry is the most profitable industry on Earth

Figure 1: The most profitable industries in 2015. (Source: Forbes).

2. Global sales of pharmaceuticals expected to exceed US$1.6 trillion in 2016, although relative rate of sales growth is declining, especially in 'developed'/industrialised countries

Figure 2. Actual and projected global pharmaceutical sales revenues to 2018. (Source: Deloitte).

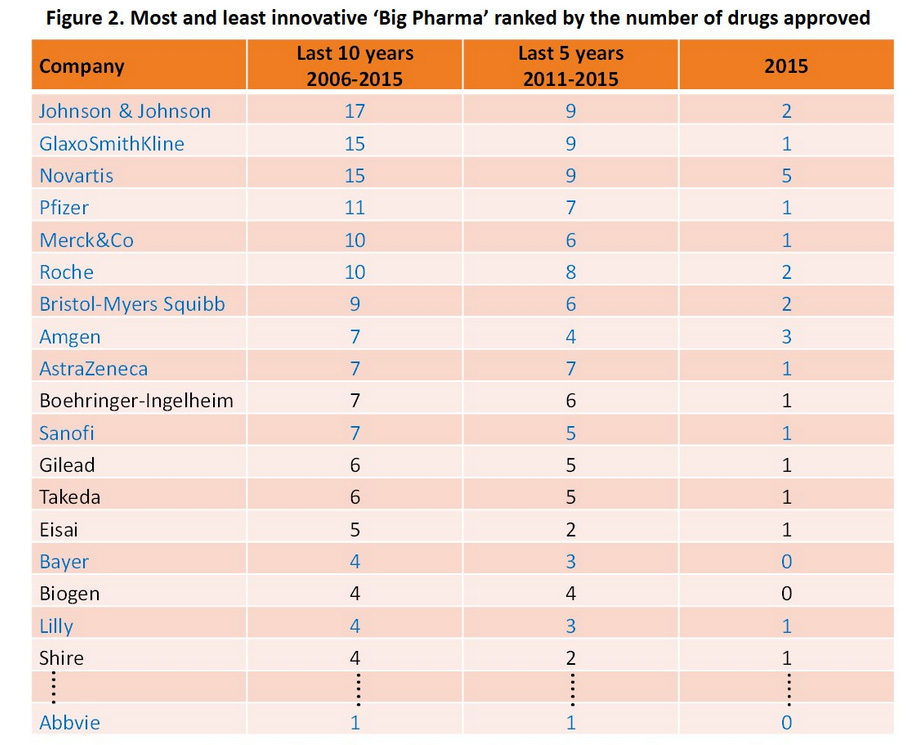

3. Innovative drugs i.e. biologics and ‘first in class’ drugs rapidly displacing blockbuster synthetics as biggest selling drugs

Figure 3. Most and least innovative ‘Big Pharma’ companies ranked according to number of drugs approved by FDA. (Source: Forbes)

4. USA, Japan and Canada show highest per capita spend on pharmaceuticals, with growth in ‘pharmerging’ markets increasing rapidly

Figure 4. Annual pharmaceutical spend per capita in selected countries and regions projected in 2016 (in US$) (Source: Statista)

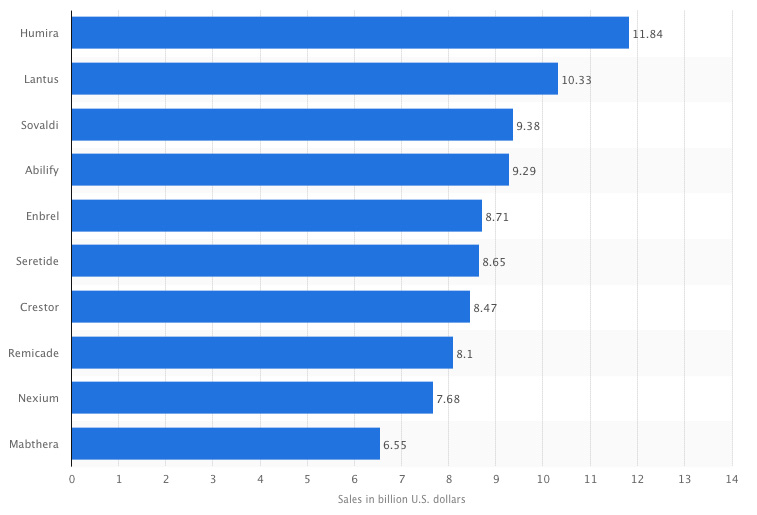

5. Many of the world’s top-selling drugs are now biologics

Figure 5. Top selling pharmaceutical products by sales worldwide (billions of US$). (Source: Statista).

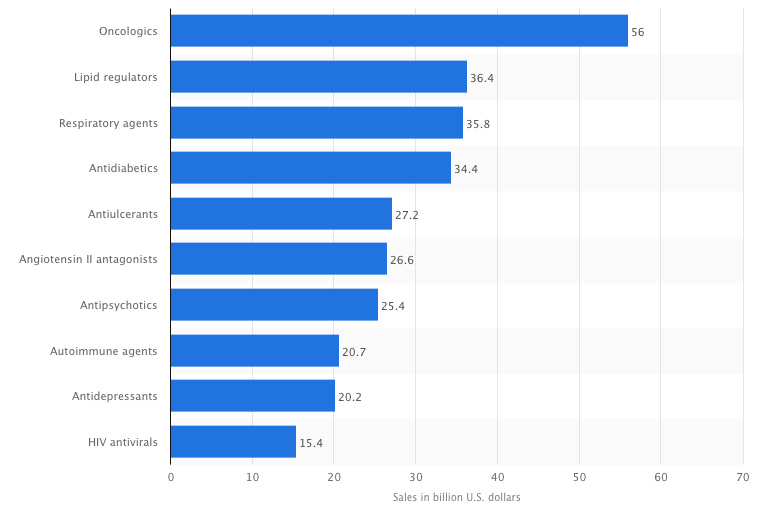

6. Among the top 10 selling classes of drugs are several with very low rates of effectiveness

These include oncologics (cancer drugs), lipid regulators and angiotensin II antogonists (for heart disease and hypertension), antidiabetics, antidepressants, autoimmune agents (for rheumatoid arthritis, lupus, Crohn’s, psoriasis, Hashimoto’s, etc.)

Figure 6. Top 10 pharmaceutical therapeutic classes worldwide in 2010 by sales (in billions of US$) (Source: Statista).

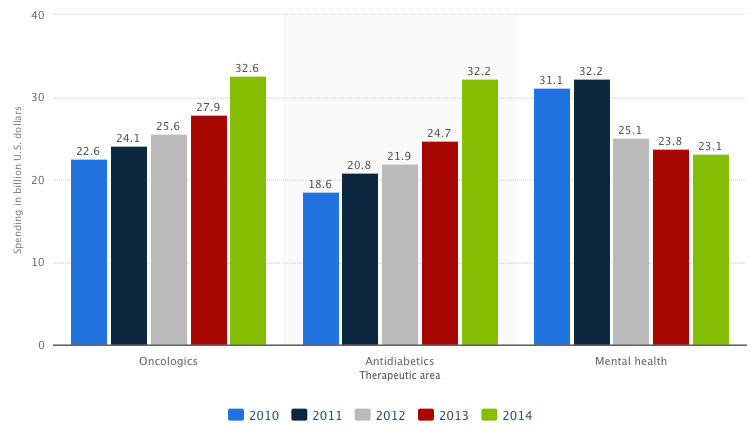

7. Sales of oncologics and antidiabetic drugs are increasing markedly year on year, despite no significant breakthrough in the drugs’ ability to cure the target diseases

Figure 7. Top 3 therapeutic areas by spending in the U.S. from 2010 to 2014 (in billions of US$) (Source: Statista).

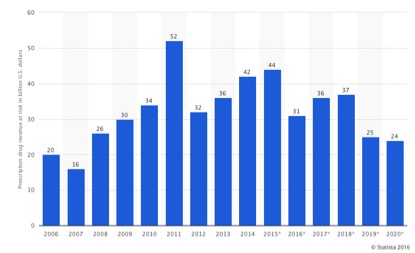

8. We’re not yet over the ‘patent cliff’: patents on over 150 major drugs will expire in the next 5 years, with US$37 billion of prescription drugs at risk from patent expiration in 2018 alone

Figure 8. Worldwide total prescription drug revenue at risk from patent expiration from 2006 to 2020 (in billions of US$) (Source: Statista).

What can we conclude?

There are several important conclusions we can draw. These include:

- Big Pharma is remarkably resilient and fairing better than some expected after the expiration of the patents of the biggest blockbuster drugs like Lipitor

- The classic Big Pharma corporations (Novartis, Pfizer, Roche, Sanofi, Merck, Johnson & Johnson, GlaxoSmithKline and AstraZeneca) are being increasingly joined by pharma biotechnology companies, altering the Big Pharma mix

- Drugs are sold less because of their effectiveness in managing or curing a disease, but more as a result of the effectiveness of the marketing surrounding particular drugs

- Sales of biologics and biosimilars are displacing classical synthetics but this is generally achieved by selling very highly priced drugs to smaller (niche) target markets

- The storm of biologics coming onto the market will increasingly blur the line between drugs and innovative natural products

- Sales in established Western markets is flat-lining, with major growth projected in the ‘pharmerging’ markets

One thing is sure; the notion that the typical doctor, trained in orthodox medicine, will reach for a diet and lifestyle solution, or an unpatented natural medicine, as a means of helping prevent or treat his or her patients is some way off. What has happened instead, is more and more people will be prescribed lower cost, generic drugs for common conditions. For more complex conditions, such as autoimmune diseases or cancer, patients will be lured towards very expensive biologics. The question will increasingly become: who pays? Inequalities in healthcare will be compounded more than they are already.

That’s good reason why it's so crucial to get the word out on how so many diseases can be managed by natural means, including through diet and lifestyle modification and judicious use of particular natural products. And that’s why ANH exists. We are passionate about protecting our right to access these approaches, as well as promoting increased adoption of these natural and sustainable approaches to healthcare worldwide. Please support us in any way you can.

Comments

your voice counts

18 February 2016 at 11:02 am

Thsanks for these very interesting data but rather hard to read the figures.

19 February 2016 at 10:12 am

Hi David,

Thank you for bringing that to my attention. I have adjusted the graphs in the article to hopefully make them easier to read.

Many thanks,

Susie

18 February 2016 at 11:07 am

The missing words in this article are regulatory capture and institutional corruption. These terms explains it all. The Pharma lobby has captured the politicians and the drug regulators who are supposed to look out for the public interest, not the continued profits of the Pharma industry.

22 February 2016 at 2:21 pm

The pharmaceutical industry is part of what is wrong with the whole corrupt system we live in. Money rules over all.

23 February 2016 at 8:52 am

Personally i would love to see a comparison between CAM and pharma in terms of profit and cost to produce medication. Would love to see the info on global sales of CAM products too.

I would also like to see some study's on the long term effects of natural products. From what i have seen it is a generally unregulated industry, with not alot of research done into safety!

Your voice counts

We welcome your comments and are very interested in your point of view, but we ask that you keep them relevant to the article, that they be civil and without commercial links. All comments are moderated prior to being published. We reserve the right to edit or not publish comments that we consider abusive or offensive.

There is extra content here from a third party provider. You will be unable to see this content unless you agree to allow Content Cookies. Cookie Preferences